Home

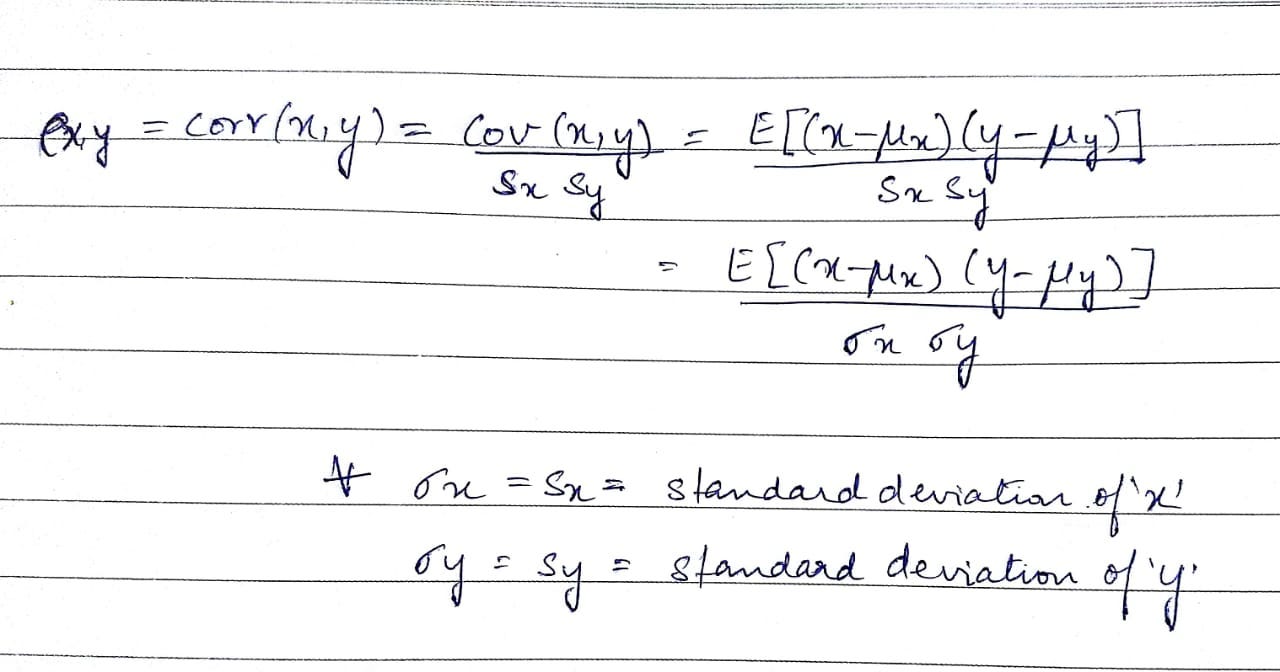

/ How To Calculate Covariance Using Correlation And Standard Deviation : Ρ (r i, r j) = corr (r i, r j) = cov (r i, r j)/σ (r i)σ (r j)

How To Calculate Covariance Using Correlation And Standard Deviation : Ρ (r i, r j) = corr (r i, r j) = cov (r i, r j)/σ (r i)σ (r j)

How To Calculate Covariance Using Correlation And Standard Deviation : Ρ (r i, r j) = corr (r i, r j) = cov (r i, r j)/σ (r i)σ (r j). How the correlation coefficient formula is correlated with covariance formula? This video illustrates how to calculate and interpret a covariance. Deviation of asset 1 and a standard deviation of asset 2. The formula for correlation is equal to covariance of return of asset 1 and covariance of return of asset 2 / standard. Ρxy = correlation between two variables cov (rx, ry) = covariance of return x and covariance of return of y

What is the formula for standard deviation and variance? Aug 26, 2019 · cov(x, y) = covariance of the variables x and y σx = sample standard deviation of variable x σy = sample standard deviation of variable y. Karl pearson developed the coefficient from a similar but slightly different idea. Correlation = cov(x,y) / (σ x * σ y) where: The formula for correlation is equal to covariance of return of asset 1 and covariance of return of asset 2 / standard.

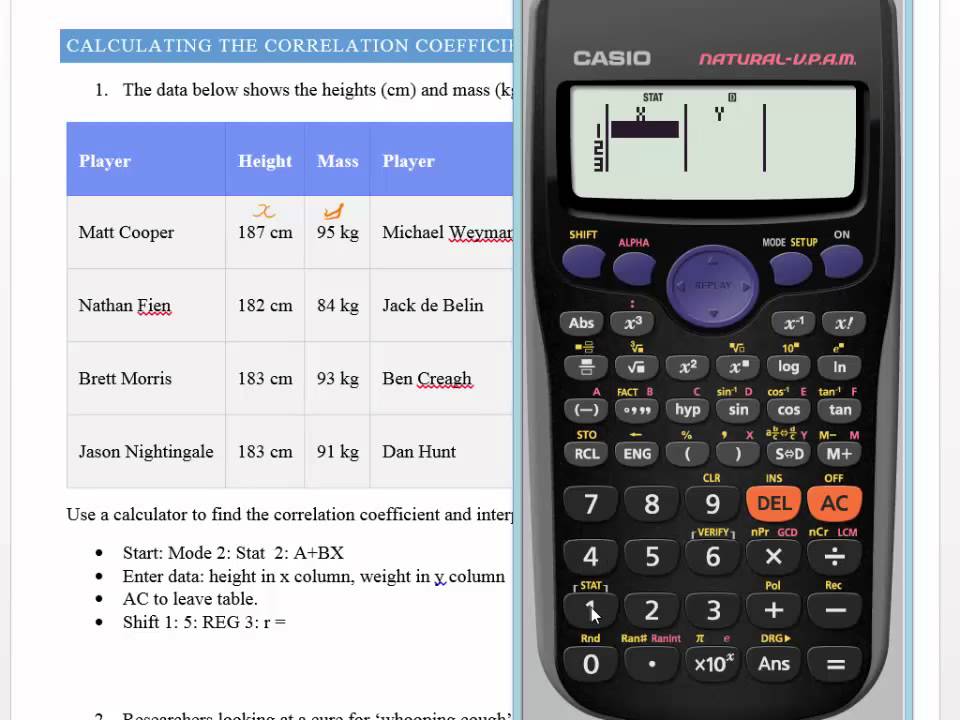

Correlation coefficient on a casio fx-82AU - YouTube from i.ytimg.com The correlation coefficient measures the strength and direction of the linear relationship between two variables. It is calculated by dividing the covariance between two variables divided by the product of their standard deviations. Covariance is equal to the correlation between two variables multiplied by each variable'. Mar 15, 2018 · how to calculate covariance the formula for covariance is as follows: Cov x, y = e(x−ex)(y − ey) c o v x, y = e (x − e x) (y − e y) the covariance between two random variables can be positive, negative, or zero. What is the formula for standard deviation and variance? Covariance of x & y variables. Deviation of asset 1 and a standard deviation of asset 2.

Covariance of x & y variables.

How the correlation coefficient formula is correlated with covariance formula? Aug 19, 2020 · the general formula used to calculate the covariance between two random variables, x and y, is: Cov x, y = e(x−ex)(y − ey) c o v x, y = e (x − e x) (y − e y) the covariance between two random variables can be positive, negative, or zero. It is calculated by dividing the covariance between two variables divided by the product of their standard deviations. Karl pearson developed the coefficient from a similar but slightly different idea. Ρxy = correlation between two variables cov (rx, ry) = covariance of return x and covariance of return of y The formula for correlation is equal to covariance of return of asset 1 and covariance of return of asset 2 / standard. Covariance is equal to the correlation between two variables multiplied by each variable'. However, cov(x,y) defines the relationship between x and y, while and. Ρ (r i, r j) = corr (r i, r j) = cov (r i, r j)/σ (r i)σ (r j) This video illustrates how to calculate and interpret a covariance. What is the relationship between standard deviation and variance? Deviation of asset 1 and a standard deviation of asset 2.

Cov x, y = e(x−ex)(y − ey) c o v x, y = e (x − e x) (y − e y) the covariance between two random variables can be positive, negative, or zero. The formula for correlation is equal to covariance of return of asset 1 and covariance of return of asset 2 / standard. Deviation of asset 1 and a standard deviation of asset 2. The correlation coefficient measures the strength and direction of the linear relationship between two variables. Covariance is equal to the correlation between two variables multiplied by each variable'.

Covariance Formula Expected Value from miro.medium.com Can standard deviation be larger then its variance? What is the approximate standard deviation of? What is the formula for standard deviation and variance? This video illustrates how to calculate and interpret a covariance. How the correlation coefficient formula is correlated with covariance formula? Covariance is equal to the correlation between two variables multiplied by each variable'. Ρxy = correlation between two variables cov (rx, ry) = covariance of return x and covariance of return of y Deviation of asset 1 and a standard deviation of asset 2.

Can standard deviation be larger then its variance?

Covariance of x & y variables. What is the formula for standard deviation and variance? What is the approximate standard deviation of? Deviation of asset 1 and a standard deviation of asset 2. Correlation = cov(x,y) / (σ x * σ y) where: Mar 15, 2018 · how to calculate covariance the formula for covariance is as follows: Ρ (r i, r j) = corr (r i, r j) = cov (r i, r j)/σ (r i)σ (r j) Covariance is equal to the correlation between two variables multiplied by each variable'. The formula for correlation is equal to covariance of return of asset 1 and covariance of return of asset 2 / standard. Can standard deviation be larger then its variance? What is the relationship between standard deviation and variance? Aug 26, 2019 · cov(x, y) = covariance of the variables x and y σx = sample standard deviation of variable x σy = sample standard deviation of variable y. It is calculated by dividing the covariance between two variables divided by the product of their standard deviations.

What is the formula for standard deviation and variance? Covariance of x & y variables. Aug 19, 2020 · the general formula used to calculate the covariance between two random variables, x and y, is: Aug 26, 2019 · cov(x, y) = covariance of the variables x and y σx = sample standard deviation of variable x σy = sample standard deviation of variable y. Covariance is equal to the correlation between two variables multiplied by each variable'.

How to calculate covariance between two stocks in excel ... from bobbewegt.com Aug 26, 2019 · cov(x, y) = covariance of the variables x and y σx = sample standard deviation of variable x σy = sample standard deviation of variable y. Covariance of x & y variables. Karl pearson developed the coefficient from a similar but slightly different idea. Covariance is equal to the correlation between two variables multiplied by each variable'. Ρ (r i, r j) = corr (r i, r j) = cov (r i, r j)/σ (r i)σ (r j) What is the formula for standard deviation and variance? Deviation of asset 1 and a standard deviation of asset 2. Ρxy = correlation between two variables cov (rx, ry) = covariance of return x and covariance of return of y

What is the relationship between standard deviation and variance?

How the correlation coefficient formula is correlated with covariance formula? Ρxy = correlation between two variables cov (rx, ry) = covariance of return x and covariance of return of y Ρ (r i, r j) = corr (r i, r j) = cov (r i, r j)/σ (r i)σ (r j) Covariance of x & y variables. Deviation of asset 1 and a standard deviation of asset 2. What is the approximate standard deviation of? Can standard deviation be larger then its variance? The correlation coefficient measures the strength and direction of the linear relationship between two variables. The formula for correlation is equal to covariance of return of asset 1 and covariance of return of asset 2 / standard. This video illustrates how to calculate and interpret a covariance. However, cov(x,y) defines the relationship between x and y, while and. Cov x, y = e(x−ex)(y − ey) c o v x, y = e (x − e x) (y − e y) the covariance between two random variables can be positive, negative, or zero. Aug 26, 2019 · cov(x, y) = covariance of the variables x and y σx = sample standard deviation of variable x σy = sample standard deviation of variable y.

How the correlation coefficient formula is correlated with covariance formula? how to calculate covariance. What is the formula for standard deviation and variance?

= corr (r i, r j) = cov (r i, r j)/σ (r i)σ (r j)){kind=link}